by MHolland | Jan 21, 2021 | Accounts Receivables, Business Tips

Two weeks ago, I talked about the timing of your sales pipeline. Last week I wrote about your cash conversion cycle…

As a refresher, your Cash Conversion Cycle is the number of days – on average – it takes for you to convert working capital to cash.

You start with the number of days it takes to collect your accounts receivable. Then you add that to the number of days it takes to sell your inventory. Finally, you subtract the number of days you take to pay your vendors.

|

Business A |

Business B |

| Days to collect receivables |

40 |

25 |

| Days to sell inventory |

15 |

35 |

|

55 |

60 |

| Less – days to pay vendors |

(15) |

(25) |

| Cash Conversion Cycle |

40 |

35 |

Quiz – which is better, Business A, or Business B?

Business B. Why? Because it takes only 35 days, compared to 40 days to convert working capital to cash.

How can Business B get even better? By managing inventory better! It is 35 days on average to sell and only 15 days for Business A.

How can Business A improve? By getting paid quicker, and/or paying vendors a bit more slowly. It is taking 40 days to collect its receivables versus 25 for Business B.

Here are 6 ways to increase your cash-flow:

Way # 1 – Order Inventory Later

Inventory is money on the shelf.

I remember touring a warehouse once, years ago, and was shocked to see so many items laying on the floor. Other items were collecting dust. I said, “you know, if those were gold bars, would you treat them like that?”

Ordering the wrong stock too soon is going to tie up your working capital.

Order the wrong stock and you have trouble selling.

Too soon, (before people need or want), and again you have money sitting on a shelf.

An example of “too soon” is buying stock for Christmas in March. That said, if you get a great deal that could be a good business decision.

Inventory management is an art. It is related to three things:

- Timing of purchase

- Ability to re-sell the inventory quickly.

- Availability from suppliers

Way # 2 – Get Deposits from Customers Upfront

I believe Dell Computers had a negative cash conversion cycle because you pay for the computer upfront. Only then do they build/assemble it for you.

When I suggest getting deposits upfront to businesspeople the response is often – “I cannot. My customers will not accept that”.

How do you know? Who sets the terms?

If Michael Dell had asked his customers I am sure they would have said – “we prefer to pay on delivery”.

Michael Dell set the rules and grew a massive global cash-machine as a result.

Way #3 – Get Accurate Invoices Out Fast

The longer it takes for you to issue an invoice the slower the payment. This one needs no explaining, right?

Way #4 – Chase Those Receivables

Once you have sent your invoices – chase them with a system.

We use software that is incredibly friendly, powerful, and consistent. It is fully automated to chase our clients receivables for them.

This shortens the days your receivables are outstanding before becoming cash in the bank.

Way #5 – Only Sell to Credit Worthy Customers

It makes no sense to sell to someone who is a credit risk.

When they do not pay, you have lost more than the receivable.

As I have written about before, you lose the entire Gross Profit on that sale.

A bad debt of $1,000 is not $1,000. Take that and divide by your Gross Profit %.

$1,000/30% = $3,333.33.

To understand the philosophy behind this, please read this blog:

Top 7 Mistakes People Make in Managing Their Accounts Receivable

Way #6 – Take a Wee Bit Longer to Pay Your Payables

If you can, pay a wee bit more slowly.

Big companies and the government are notoriously slow payers to their vendors.

Develop a policy. Too many businesses just pay, well, whenever. The “whenever” is when a vendor screams loudly!

By all means, pay small vendors faster. For bigger ones, certainly pay a couple of days before due. Not sooner. BC Hydro will not need your money early. Pay it close to the due date.

Conclusion

Doing the above 6 things will lower (remember less is more) your cash conversion cycle.

Thanks for reading…

by MHolland | Sep 9, 2020 | Business Tips

Why do we start a business?

To make money? Is that it? Is that ALL there is? Could there more to it than that?

Make new friendships? Have fun? That sounds a little more “user-friendly”!

Go a bit deeper and look.

Do we want a legacy? Yes? If so, how do we do that?

And what is a legacy? Is it the structures? The people? Or something more intangible?

Everything You See Will Disappear

Take a look at your business. Look at the buildings, offices, computers, the people. Think of the systems, the products you sell, the services rendered. Imagine the computers, the software, your website.

It will all disappear. All of it.

You will be gone. You may leave your great business to your kids or a successor. They will die and be gone. They may leave it to their kids. Ultimately, they, too, will be gone.

This is just the nature of everything we see. It is all created stuff destined to disappear. To fade into the source that it came from.

Take a look at this picture. John, one of my best friends, did it. Beautiful, isn’t it.

And, what a delightful symbol. We all see the water right behind it. The tide will come in and sweep it away. Back from where it came.

That is your business.

Feeling freed up, or despairing?

I hope it frees you a bit from the grip of control we all – as business owners – can have on our businesses. (Or the business controlling us)! We created our businesses and we want to be proud of them. We WANT them to last! To leave a legacy…

But wait, there is one thing that lasts…

I will come to it, keep reading.

Buddha Art

There is a style of painting called “Buddha art”. You start with a blank canvas, water, a brush, and evaporating ink.

You draw a beautiful painting. The water evaporates and the canvas turns blank.

Can we hold our businesses so lightly? Creating them as art. Letting them fade and re-create them daily?

How does that image make you feel? Less stressed, I hope…

Saint Theresa of Lisieux

Saint Theresa entered a Convent in France at the age of 15. She died at age 24. She lived a simple life. St. Theresa did not create an order, nor start a business, or a publishing house.

What she did do – and she is a great example for us – is this. She decided to love her fellow Sisters with all her heart. She did every small thing – washing dishes, sweeping the floor, serving others – with love. With love, she transformed a relationship with a grumpy older nun into a loving, caring one.

When people visit the convent, they are absolutely shocked at how small it is. They imagined a large Convent at the center of acres of gardens. No, it was tiny.

What is remarkable about her life is that she wrote so little. She was not ambitious in the physical sense. Yet she touches the hearts of millions through her book, “The Little Way”. She is a Doctor of the Church. One of a small few.

What has this got to do with business?

Legacy. Her legacy lives because she did small things with love.

Are we trying to conquer the world with our stunning acumen, great systems, brilliant competence?

Where is the love? The kindness?

“Our days on earth are like grass; like wildflowers, we bloom and die”.

Your Business Legacy

Your business legacy will be how much you did each act with love.

That is all that will remain. The tide washes the mandala back to sea. The ink disappears on the ink painting. In your business, what remains is the love you put in.

Imagine doing each act, each day, with all your love. How you talk to your team. The way you interact with your clients. An email dripping with softeners and kindnesses.

Build your business with skillful finesse and let that skill overflow with love.

The chances the “things” of your business will last a wee bit longer than the sand mandala above expand in direct proportion to the love poured in.

And who will we all become in the process?

Thanks for reading…

by MHolland | Sep 4, 2020 | Business Tips

I am almost finished reading an awesome book called Hyper-Focus by Chris Bailey.

Some of what I read I knew already. Keep reading and I will share some cutting edge pointers.

The stats he refers to are incredible. One study was done in situ – meaning live studies on real workers.

(In situ studies are rare. It took them 6 years to get permission, Why? Potential disruptions to the live workers).

They attached monitors to the workers to regulate heart rate for stress. Monitors were added to their computers. This was to see how often people switch from app to app, task to task.

Wanna know how often? Ready for this? Every 40 seconds. The average worker switches every 40 seconds from task to task, app to app.

That is stunning. How does any real, concentrated work ever get done?

Here is another stat. Let us say that you are in a hyper-focused state. You get interrupted. It takes an average of 22 minutes to get back to where you were before the distracting interruption.

Yikes!

You may be wondering what exactly is hyper-focus?

First, you will be working on a project that is challenging. Yet not too complex. It cannot be done habitually.

You will enter a state of flow. An hour whizzes by like 15 minutes. You forget to eat. No distractions (or few) are entering your space. That includes your workspace, your mind, your emotions.

At the end of a session of hyper-focus you feel energized, not tired.

The kicker – you get a LOT done and done well!

Here are my top 3 tips so far…

Number 1 – Buy an App to Stop Distractions from Bombarding You

Your smartphone is not a phone. Consider it is a very annoying computer in your pocket. Annoying because it is harping notifications all day long.

New email. Ding. New text. Ding. New WhatsApp. Ding. New call. Ring-ring-ring.

Ok, you may have turned off notifications and that is one step forward for sure.

I just bought an app/service called Freedom. Good name.

It is designed to stop the addictive pull to check emails, answer the phone, check WhatsApp or social media threads.

There are a few programs like this out there (Cold Turkey, Rescue Time). So far, I like Freedom the best.

What the app does is set up a distraction free environment. It blocks all sites and apps across all your devices (phone, tablet, computer). Or you choose which apps you want blocked.

Then you set the time. I use 90 minutes to enter into a highly productive hyper-space block. You could start with any block, say 30 minutes.

You can block groups of sites. One is news sites. Try to bring up BBC News – blocked. Shopping sites can be blocked. No getting into Amazon when in hyper-focus time.

Outlook can be blocked. Multiple phone apps can be blocked.

Think of it. For 90 minutes – no emails, no texts, no messages. No unconscious checking the news, or Facebook.

Number 2 – Set Intentions

One tip Chris talks about in the book is the Rule of 3.

Focus on only 3 top items/intentions for each day. (The mind cannot hold much more than that!)

(I have practiced this and it works)!

Set your intention(s) for the hyper-focus block you set. This would be something important that forwards your business, life, or work.

As your mind wanders (and it will), keep pulling it back to your stated intention.

Chris talks a lot about Attentional Space. Doing complex, new tasks, or problem solving requires a huge load of brain power.

You cannot multi-task in a hyper-focus state.

By the way, you can multi-task – when it does not require concentration and what you are doing is habitual.

Consider most people can walk, chew gum, and carry on a meaningful conversation at the same time.

Number 3 – Take a Fast from Social Media

Facebook is designed to keep you in a loop. An unproductive, endless loop – feeding you news and ads based on your comments and views.

It craves your attention. And what do you get from it?

Come on, be honest? New, meaningful relationships? Improved, deeper relationships with your Facebook friends? More clients for your business?

Facebook and Twitter – all of these types of software – are black holes. And you are not in control. You may even be addicted.

Take a cleansing, purging bath from social media for 30 days. Too much? Try only using them 30 minutes a day max.

Give it a go.

This book is chock-a-block full of great tips and studies.

By the way, the second one-half of the book is dedicated to scatter focus.

No one can hyper focus ALL the time. You get the most done in Hyper Focus. But you are most creative when in Scatter Focus time.

Here is a link to Amazon for the book:

HyperFocus by Chris Bailey

by MHolland | Jun 25, 2020 | Business Tips

Increase sales by cold calling? You would rather stick needles in your eyes, right?

Seasoned sales pros hate cold calling. Did you know that? It is true.

They do it because they think it gets sales. And cold calling does work. The problem it that it is a brutal game. Loaded with rejection. Doing it means you have to build up a steely shell and an iron will.

I have done it. Smiled and dialed my way through lists callings hundreds a day. Yes, you read that right – hundreds.

In fact, during that time I was using Skype. Being clever with Excel I discovered I could click a number in a cell, and auto-dial using Skype. I also found out – to my utter shock – that Skype has a “fair use” policy. (Unlimited does NOT mean unlimited). I was calling so many people that I got a very nasty email from Skype. (Thank you Microsoft). It said, in scary legal terms, to “cease and desist”. Or they would ban me from using Skype. Forever. No warnings even!

Ok, that is a story for another day. Today I listened to a fantastic business podcast on cold calling. (I will share link below).

Here are some tips I gleaned:

Tip #1 – Cold Calling is NOT a Numbers Game

Yup. Not a numbers game. Wait a minute. Since the invention of the phone has not this been common knowledge?

Commonly believed does not equal common sense.

Here is the problem. A big list is not a targeted list. You will end up calling a lot of non-qualified leads.

I have bought lists from list brokers. I made the mistake of thinking it was targeted. These bought lists were casting too big a net.

In the podcast the expert, David Walter, says something different. Only call very targeted leads.

Here is the example he gives. The boss tells the sales guy to – “go out and make calls”. They make calls. More calls = more sales.

The boss tells his Executive Assistant: “go get in touch with John’s attorney”. That is what he/she will do.

See the difference? One is shotgun. The other a rifle.

This leads me to…

Tip #2 – You Are Selling to the 80% That Are Happy with What They Have

What? How do you sell to the 80% that are happy with what they have? Makes no sense, right?

If you are like me, I bet you thought you are scouting for the 10% that are unhappy with what they have, correct? (The other 10% are just rude and will hang up on you).

How the heck do you sell to the 80% that are happy?

Because they do not know any other way than the way they do it now.

What you say is (as example) something along these lines –

“I know you are probably very happy with what you have in the area of ______, am I right?”

Then the punchline: “as a businessperson, I bet you like to keep your options open, yes?”

You are looking to set an appointment (or online demo) to show them another way. A way that is better, cheaper, faster, stronger than what they have! (You get the idea).

Tip #3 – Never Leave Voicemail

I did some cold calling the other day. I left some voicemails.

The challenge is – I now have zero control. What are the odds they will call me back? Zip.

What you do is this:

…you call the same targeted person – over and over – until you reach them. Three times a day if needed.

Do not leave voicemail.

In Summary

There is much more in the podcast than what I wrote above.

In these tough times when you may want to add more sales, try calling the prospects you want as clients.

Take a listen:

Why Cold Calling Goes Wrong

Thanks for reading…

by MHolland | Jun 18, 2020 | Business Tips

I just read a Blog from the Business Development Bank of Canada called 7 Steps to Setting the Right Price for Your Products or Services.

The Blog makes some good points. I have 2 comments on it, though.

Firstly, the Blog has the overall wrong focus. It is inward not outward. This is common.

What do I mean? In this BDC Blog the first two steps are:

- Calculate your direct costs;

- Calculate your Cost of Goods Sold.

Those steps are important, but not yet.

Your internal costs should not dictate your prices.

Yes, you read that right.

Why? No one cares.

Think about it. When you shop, do you care if that store is either:

- Losing money on that thing you just bought? or,

- Making a killer profit on the sale?

No difference, right? You are looking at one thing only – value for money.

And, that is subjective. It varies from person to person. Place to place. Time to time.

This leads me to the first thing you must look at in pricing….

What Do People Value in Looking at Your Products?

Why do they shop with you? Is it unique? What makes it unique?

Let us look at two simple examples –

First, things have subjective value. There are a group of consumers who value the 3-point star on a Mercedes-Benz. It is a symbol of quality. General Motors could replicate the exact same car as a Mercedes. Those same people would value it less. In this case, it is the prestige of that 3 Point Star on the hood. It may be a sense that the inherent quality means the car will last longer. Ergo, it is worth more.

Secondly, bundling can create a perceived value. You have never skied before. You go into a ski shop to buy a pair of skis.

The astute salesclerk guides you to a “Beginner Ski” package. It includes pants, jacket, boots, poles, toque, gloves, and goggles. You went into the store to spend $xx and ended up spending 3 times that!

There was a perceived value. The single price of each item likely added up to more than the bundle price. Yet, the store owner made a much higher sale.

OK, so we know value is a perception. It is not objective. If it were, everyone would have the exact same reaction to the sticker price of an item. We know that is not true.

This leads to the second thing…

No One Cares About Your Costs

You enter the store, and the owner sits you down. He pulls out his Profit and Loss Statement, showing you all his costs. He explains how expensive it is to be in business these days. Yawn.

He shows you a modest and fair markup for his products.

Feeling good yet? No?

Why not? His markup is fair. It is even lower than you would expect.

You just do not care. Why not?

Because for one thing, he could be a poor manager. His staffing costs could be way too high. Material wastage is out-of-control.

I repeat. The store owner’s costs have no bearing on your buying decision.

With one exception! Buyers are acutely aware of abusive labour practices. Unfair labour practices can bring a decline in that perceived value.

This leads to my last point…

Lower Costs Does Not Equal Lower Price

You figure out a way to make your products for less. Lowering your prices is the ethical thing to do, right?

Deciding to lower prices could increase volumes. Or, invite more competition.

People value the end result of what you offer them. Your lower costs does not change their perceived value.

One of the points in the BDC Blog was to determine your markup from your actual costs. The problem here is obvious. Why should your customers pay for excess fat in your production?

Or, you may be leaving profit on the table they would be happy to pay for.

In Summary

There is nothing wrong with low prices, low costs, high volume. The challenge is that you are competing with Costco, Amazon, and Walmart. And, you will not win.

I just read about a hardware business in the USA. The owner sent his team members to Lowe’s and Ace Hardware to check prices. He would then lower his. A better strategy would be to stock unique hammers and charge more, not less.

Here are the steps in the correct order:

- Determine the value you offer through the eyes of your customer;

- Set your price;

- Look at your costs. Too high? Sharpen your pencil. Consider outsourcing your production.

Thanks for reading…

by MHolland | Jun 5, 2020 | Business Tips

Being in business is just about creating and selling stuff. Delivering services. Right?

Wrong. It is about creating advocates for your business. There is a pathway to creating advocates. It is narrow and uncrowded.

Would you like to know what it is?

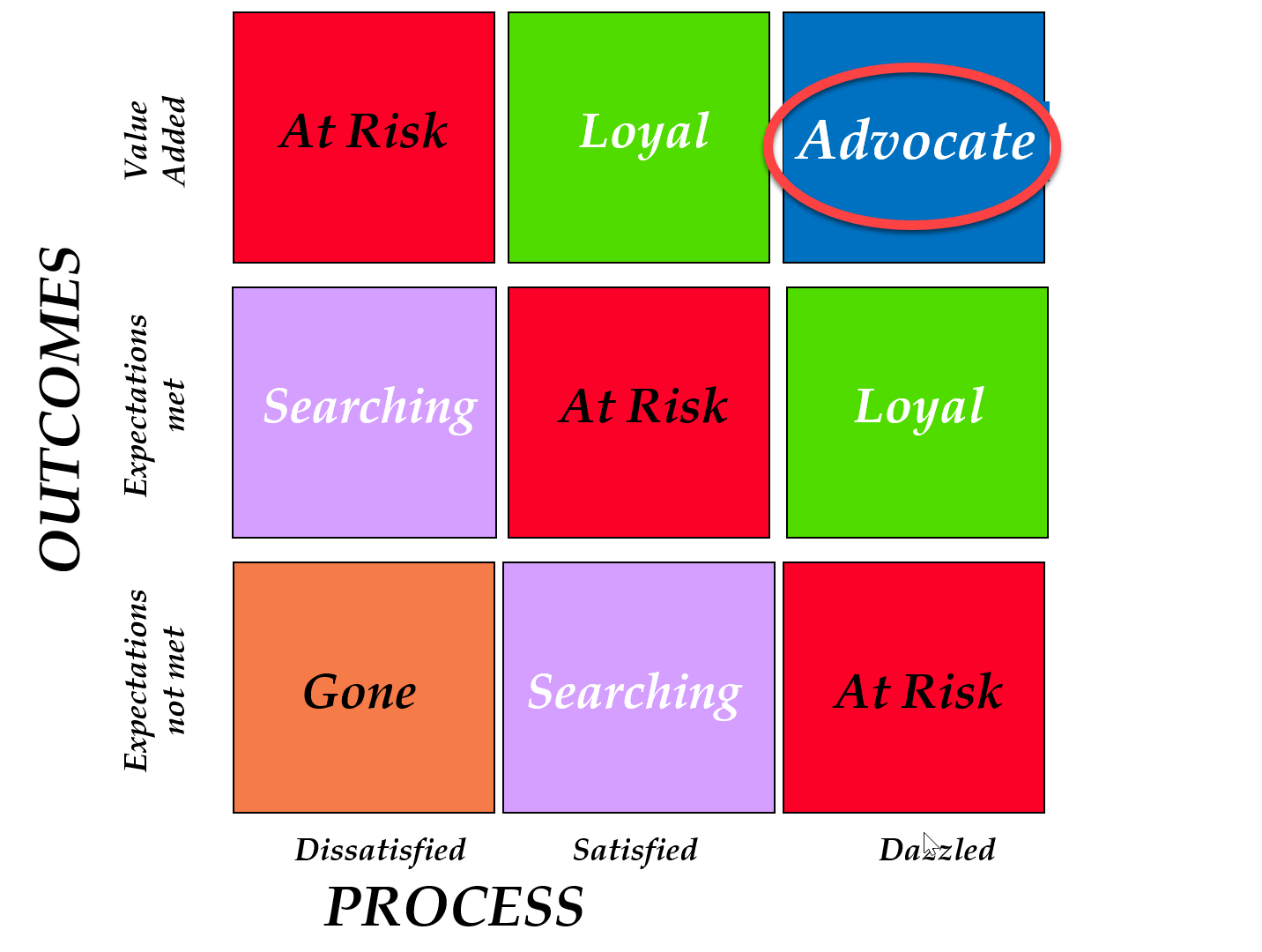

The best way to show you is with a Chart, a grid.

It looks like this:

The vertical axis is what you do – your outcomes. A law firm provides legal services. A restaurant? Meals. Clothing store? Clothes. You get the idea.

The question going up the chart is – did I ‘not meet’, ‘meet’, or exceed my customers’ expectations?

You go to a restaurant. Your meal was either crappy (not met), good (met), or just like mom’s cooking (exceeded).

Now look at the horizontal axis. It is called “Process”.

It is not how you do what you do (that is operations). It is how you deliver what you do.

Everyone knows you can get a great meal, and lousy service. It can be lousy in any number of ways.

A grumpy, rude, indifferent, or distracted server for example.

The “process” part is the people part. Did the business show they cared for you?

The Colors Are the Clue

Look carefully at the Chart above. The colors are a clue. There are 3 red boxes, 2 green, 2 purple, 1 brownish, and 1 blue.

Let me unpack it for you.

The Color Brown

The bottom corner – in our restaurant example – means the food is bad, AND the service was horrible. You are gone. And, likely you will tell a lot of people. Way more than when it is great.

The Color Purple

Look at the 2 purple boxes next. In the bottom, middle box the food is bad, but the server was friendly. (Expectations not met, satisfied with the service). In the middle, left box the food is good, and the service is horrid. (Expectations met, dissatisfied with process).

What do you do?

You are searching. You want a better restaurant to go to. Perhaps you are not gone – just yet – but actively looking!

The Color Red

Three boxes are red. Bottom right red box – you are dazzled with service; food is really awful. In top left red box – the food was terrific (better than expected), but the server was rude.

Middle red box – everything is good. Not great. Good. Food is good. Service was good. You are satisfied. Just not running home to share with your friends and family about the place.

As the business owner of this restaurant, are you secure?

No. You are “at risk”. Those customers could leave you. They will leave you when something better comes along.

The Green Boxes

There are two possibilities here. Either the food was amazing, and the service good. Or, the service was dazzling, and the food was good, not great.

You are safer here indeed. Because you have something all businesses long for.

Check it out below.

You have loyal customers.

So, what is wrong with that? Isn’t that enough. Sure. It is good. But is that what you really want? Because there is one piece missing. One secret ingredient.

Remember what I said at the beginning? The road is narrow and the gateway is small.

This leads us to the last box….

The Blue Box

The blue box is where your advocates live.

In this lonely top corner box, you have been blown away with the meal AND the service dazzled you.

And here is the lesson. The one thing advocates do (something even loyal customers do not do) is this:

- They cannot stop talking about your business

They are a walking, talking billboard for your company. They rave about you to friends and family and on social media. Stories are shared about you – good stories. They smile telling their friends about their experience. They gush a bit.

Here is the challenge (for all of us in business). Not how we get there. We may be able to pull that off – occasionally.

It is how do we stay there. How do we embed that dazzling experience with outstanding products/services into the DNA of our systems?

Thanks for reading….

PS – the above distinction applies as much – actually more – during a pandemic