by MHolland | May 21, 2020 | Accounts Receivables

Selling on credit is risky…

Businesses closed in the pandemic. Meaning they cannot pay you. Or, you cannot reach them, as offices closed.

What to do?

Three things.

Number One – Re-Set Your Credit Terms

It is better to have no sale than a bad debt.

A bad debt is awfully expensive. It is not just the cash loss. It is the recovery cost.

Imagine you have a 30% gross margin percentage. This means if you sell something for $100 that item cost you $70 ($100-$70 = $30). $30 divided by $100 = 30%.

With me so far?

A bad debt of $6,000 translates to $20,000 in new sales required to re-coop it.

Do the math. $6,000 is lost – the bad debt. Divide that by 30% to get $20,000.

Now work it backwards. You sell $20,000 x 70% in costs = $14,000. Subtract your costs of $14,000 from $20,000 in sales leaves you with a gross profit of $6,000, or 30%.

That is what you must do in sales to get back to where you were before the $6,000 bad debt.

I hope that makes you cringe a little.

Re-set your credit terms. You get to say. If your customer refuses, they do not want to do business with you.

Number 2 – Chase More Aggressively

Go after those accounts owing fast.

Call days after you send the invoice. “Did you receive my invoice? By when can we expect payment?”

Use a system to chase them with persistent and professional emails.

We use a software program for our clients designed to do only this.

And, it works. Our clients have lower “days receivable” as a result.

Follow up aggressively, and persistently.

Following-up for sticky ones should be done at the highest level. The owner.

Why? No one feels the pain more of that loss than the owner. That pain will come through in the “tone” on that call.

Number 3 – Do not Use Your Bookkeeper to Make Calls

Your bookkeeper is a bookkeeper. They like bookkeeping. Making calls is not fun for them. Why? They are introverts.

You can force them to do it.

Remember, they did not set your credit terms; nor do they choose your customers.

How can they possibly be responsible for collections?

There are professional accounts receivable collection experts. You can hire an expert in-house. Or, you can outsource it.

Outsourcing is not cheap – usually a percentage of the amount collected is billed.

To Summarize:

- Update and tighten up your credit terms

- Aggressively pursue amounts owing to you. Use a system for email chasing. Follow-up with phone calls

- Use a professional – not your bookkeeper. Or you, as the owner, make the calls.

Thanks for reading…

by MHolland | May 13, 2020 | Cash Flow

We are in the midst of a global liquidity shock.

What is that? It goes like this. Business A is not getting paid. To preserve cash they stop paying their payables.

Business B is Business A’s supplier. Business A’s account payable is Business B’s “accounts receivable”.

Business B, in turn, tells its suppliers that “no one is paying us!”. So, we cannot pay you. Ouch.

Business C (customer of Business B) says the same thing to its suppliers…

…and so on, and so on, and so on…

It is a Global Liquidity Shock.

To manage your cash-flow you must know three things it is made up of.

First Thing – Cash-Flow From Operations

You sell stuff. You have expenses. The difference is your net profit. So far so obvious…

Imagine you sold only for cash. You paid for things only with cash. Your net profit would equal your operational cash-flow.

That is not what happens though is it?

People do not all pay cash. You do not pay all expenses with cash.

Accounts receivable will become cash when collected. Inventory becomes cash when sold.

Accounts payable and other things you owe will use cash later on.

The first section of your Cash-Flow statement is called Operational Cash-Flow.

You begin with “Net Profit”.

Did “accounts receivable” go up from last month? Subtract the difference from net profit. You have not received that money yet.

Did “inventory” go down from last month? Add the difference to your net profit. You sold stuff.

Have your accounts payable gone up? You have not paid all your bills. Add the difference to your net profit.

Rule # 1 : every current asset that goes up you subtract that from your net profit. Every current asset that went down you add that to your net profit.

Rule # 2 : every current liability that went up you add that to net profit. Every current liability that went down you subtract that from net profit.

Rule 2 is the exact opposite of Rule 1.

Here is a sample Operational Cash-Flow:

| Net profit |

$6,000 |

| Accounts receivable went up |

(600)* |

| Inventory went down |

900* |

| Accounts payable went up |

3,000** |

| Operational cash-flow |

$9,300 |

|

|

*see Rule #1

**see Rule #2

Part 2 – Investing Activities

There are other things that affect cash-flow that are long-term. Buying fixed assets is one example.

You take the Operational Cash-Flow as above. And deduct the investment in long-term things like fixed assets.

It looks like this:

| Operational cash-flow |

$9,300 |

| Purchase of equipment |

(6,000) |

| Loaned money to another company |

(3,000) |

| Cash-flow before financing activities |

$300 |

Part 3 – Financing Activities

Now, you take your Cash-Flow before Financing activities as above. You add or subtract things like long-term loans and shareholder dividends.

These include long-term loans and dividend payments to shareholders.

You start with your cash-flow before financing activities as above:

| Cash-flow before financing activities |

$300 |

| Long-term loan from bank* |

6,000 |

| Dividends to shareholder |

(2,100) |

| Cash-flow before financing activities |

$4,200 |

*you financed the equipment above assets

3 Cash-Flow Tips

- Push hard (with kindness) on accounts receivable collections. Use software to chase outstanding invoices. Make calls. Document everything.

- Extend payments on accounts payable. Work out payment terms with your suppliers.

- Finance equipment with long-term loans.

Thanks for reading…(if you need help, private message me)

by MHolland | May 7, 2020 | Business Tips

Everything is going virtual, right? Zoom meetings. Cloud-based accounting. Online banking. VOIP phones. Website portals.

The pandemic has forced businesses to figure out new ways to work online.

How do you market right now?

Tip #1 – Create an Awesome Service Experience Online

Let us say you own a restaurant. It has been forced to stop due to Covid 19. First question is – can you shift to takeout or catering?

How do you create an awesome service experience online?

First, look at all the points where your customer “engages with your business”.

In a restaurant these touch points are:

- Phone

- Website

- Email

- Waiter/waitress

- The Food

- Parking lot

- Front entrance

- Host/Hostess

- Physical layout

- Bathrooms

Moving the restaurant online, the touch points are:

- Phone

- Website

- Email

- Delivery man/woman

- The Food

- Packaging

- Extras

- Cleanliness of delivery vehicle

See the overlap? Five are the same. Three are new touch points.

Now, walk through each touch-point and re-engineer this business for awesome experience.

This could include:

- A re-designed website, with the daily menu and specials on the front page.

- An online-order-portal. This is where customers order and pay.

- Spiffy branded uniforms for the delivery people.

- Branded, colorful packaging.

- Training for the Team in scripts you want said as you deliver food.

- Scripts for answering the phone.

Systems for phone answering are critical. Answering the phone on the second ring – every time – creates consistency. Consistency at this time wows people. This has them keep coming back.

Tip #2 – What is Old Can Become New Again

Marketing can be offline. You can be bold and try “new” things.

When everyone is marketing online, try something old: direct mail.

Direct mail may surprise prospects. They are not getting much mail. Odds are they may read your letter.

The big challenge is a lot of businesses are working from home. Where to send your mail? Getting the right address will be crucial.

Direct mail must be followed up with a phone call.

My coaching is trying a small number to start (25-50 leads). Then call each one the following week.

Take a problem solving, non-salesy approach. Few businesses want to be sold to in a pandemic. Do you have a service that can fix a problem or save them money? They may be eager to listen to you.

I hope this helps. Thanks for reading…

by MHolland | Dec 11, 2019 | Business Tips

Many people might answer the question above by saying, “to make a profit”.

After all, why else would you be in business, if not to succeed and make a profit?

Fair enough, however, consider in another area of your life – health. Would you ever say, the purpose of my life in the area of health is to lose weight?

Losing weight and earning a profit are simply results of doing the right activities.

I would like to suggest that all businesses could have the same over-arching Strategic Purpose that is composed of 4 parts.

I can hear the groans already! What! The same Strategic Purpose as all other businesses?? How does that work? My business is unique, I can hear you saying…

Hang on, you are right, your business has a very unique strategic focus.

The 4 Purposes of a Business I am about to share with you are the umbrella that you hang all the specific things you will do to achieve your overall purpose.

Purpose #1 – To Create New Customers

If you are not in business to create new customers, then what are you in business for? Certainly, I am sure we can all agree that creating new customers is valid for all businesses.

Now, you will uniquely apply your creativity to figure out specifically how you will create new customers.

There are only two realities here – either you have nothing to sell, or you do, yet cannot convince people to buy it for any number of reasons – price, quality, need, timing, workability, competition and so on.

Ok, I know this is very basic, yet you must have a way to create new customers, or you don’t have a business.

Purpose #2 – To Make Sure They Keep Coming Back

Now, you have created new customers, how do you make sure they keep coming back?

Some businesses (no one reading this!) are like revolving doors. A customer comes in the front door and leaves, never to return, out the back door.

They leave, at about the statistically proven rate of 7/10 if they perceive you do not care.

Here, to ensure they keep coming back you must offer great products and services at fair prices, together with great service and incentives to make sure they keep coming back.

Can you see where this is going? It is not enough to create new customers; you must ensure they keep coming back.

Also, you can start thinking of how to ensure they keep coming back! Your own unique creative ways.

Purpose #3 – To Turn Those People into Advocates for You

Now it is getting progressively more challenging. To get customers coming back more often is one thing, to turn them into advocates for your business is something entirely different.

First, what exactly is an advocate?

An advocate is someone who is a walking billboard for your business. They love the service so much that they don’t just come back, they cannot stop talking about you.

Can you think of a business that you use as a supplier, or perhaps are a retail customer of, that you rave about? You literally cannot help talking about that business. It takes more to create advocates than just having great products and services. It takes more than having awesome service.

You have to exceed your customers expectations in both the core product/service of your business and also in how it is delivered – the soft skills in customer service delivery.

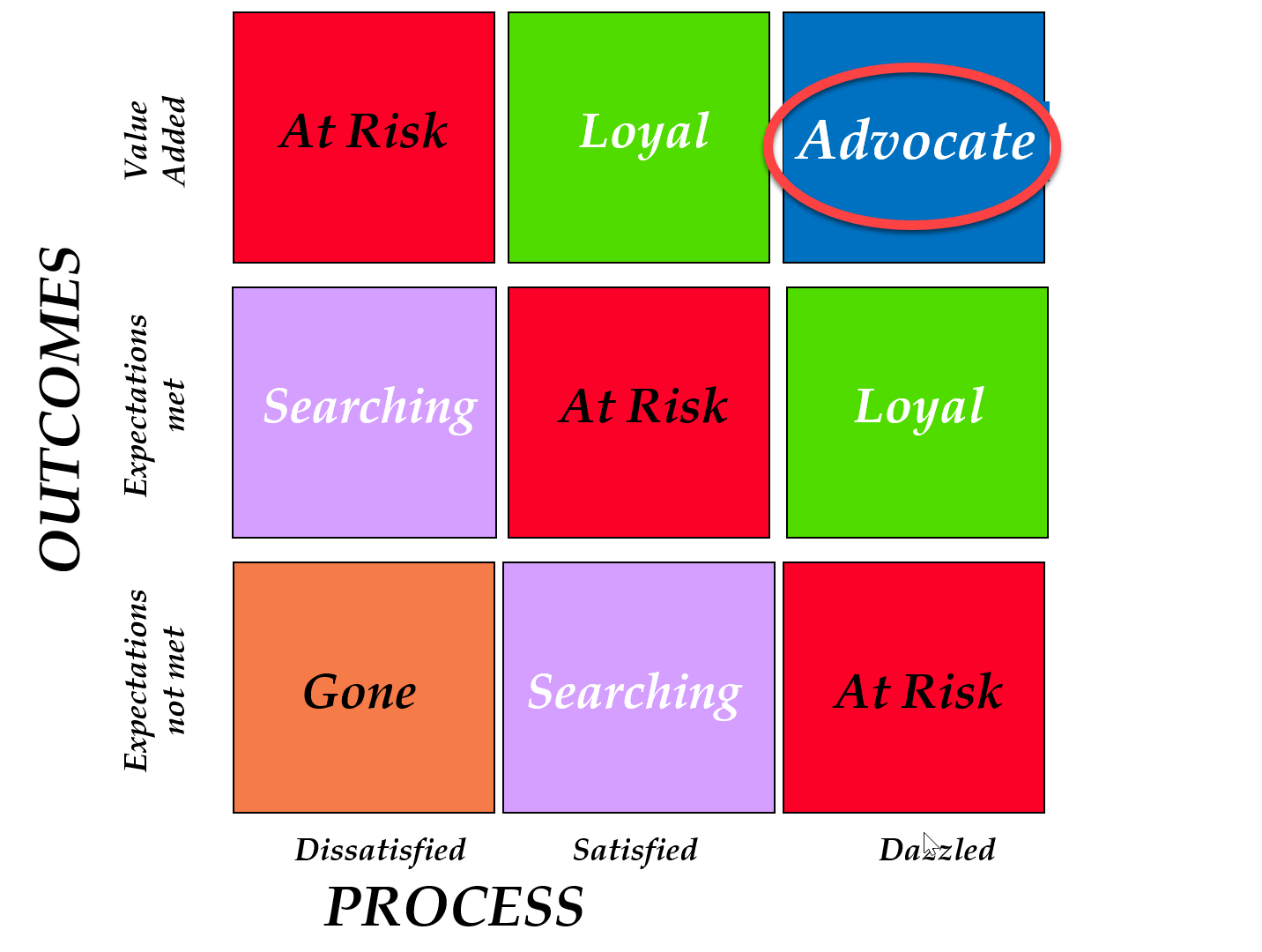

Take a look at this Chart below to see the rarity of it (only one box is reserved for it):

Starting at the bottom, if you do not meet your customer’s needs and they are dissatisfied with the service, they are “gone”.

They are searching for an alternative to your business when the service is satisfactory, but their needs are not met, or they are met and the service sucks.

You are “at risk” of losing them when you have added real value in your products or services yet service is bad, or if you have “just met” their expectations and they are “just satisfied” with the service, or lastly if you even dazzled them with awesome service yet the outcome was not met (shoddy product).

You can have loyal customers when you add extra value beyond “needs met” and satisfy them with service, or if you met their outcomes and dazzled them with great service.

The only box in the top right, reserved for your advocates, comes from exceeding their expectations in the outcome of the actual product/service and you coupled that to dazzling service.

Once you have that, you will need to spend very little on marketing because your customers will be raving all over town about your business…

Purpose #4 – To Have Fun Doing What You Do

If you and your Team are actually having fun (and that too is unique to each business) combined with the above three purposes, you will be rocking.

You will be adding value to your Team Member’s lives, your customers will sense the vibe of your business and be attracted to your special flavour of fun.

Having fun does not mean being childish or having a Foosball game in your office. For you it could mean an inner sense of joy bubbling through, with light-hearted humour, care, and love for your Team.

It could be the family atmosphere you created with your Team.

In Summary

Creating new customers, keeping them coming back, turning them into advocates for your business, and having fun doing all that will be a very creative and unique challenge for you to solve for your business.

Can you also see how powerful that is, and that by doing this you would be pretty much assured that the profits are a result of taking actions in these 4 areas?

Thanks kindly for reading…

by MHolland | Dec 10, 2019 | Business Tips

Kindly note the word “conservatism” in accounting has absolutely nothing to do with whether you vote conservative, liberal, or NDP! Ok, now I’ve got that out of the way, let’s define what it means in accounting.

Conservatism in accounting simply means this – that revenue is recognized only when it is assured of being realized (you could say in simple business terms – will I get paid?), and expenses are recognized sooner when there is a reasonable possibility they will be incurred (in other words, you will be liable to pay).

In other words, a cautionary approach is taken which creates more reliable financial statements for users.

Which is why I hate deferred expenses, as I wrote about in a prior Blog. People rationalize deferring expenses (putting on the Balance Sheet as an asset, rather than expensing on the Profit and Loss Statement) by applying (mis-applying?) the matching principle.

As a refresher, let’s talk about what a deferred expense is. A deferred expense (as opposed to a prepaid expense which is different. I will explain later) is an expense that was incurred now, that you think will have a future value in your business. So, you move it off your Income Statement to your Balance Sheet. In other words, you “defer” it to a later date. Sometime in the future, you will expense it.

When you don’t apply the “conservatism” principle in accounting what happens is you end up creating financial statements that cannot be relied upon. They end being full of assumption-based not fact-based.

Let us see how this works by examining a Balance Sheet…

Every Item on Your Balance Sheet Tells a Story

If you were to go through every line item on your Balance Sheet you could tell me a story about it.

Really, you could. The story would either be a true story, based on verifiable facts, or it would be a made-up story, a fairy tale based on assumptions and projections or crystal-ball gazing.

The true stories you could verify. The fairy stories you would have to spin a tall tale.

Let’s go through some examples…looking just at the asset section of your Balance Sheet.

First, what is an asset?

An asset is something you own, something that has value. I could add more distinctions, however, let’s keep it simple for now.

Cash in the Bank

Together as we go through a Balance Sheet we start with “Cash in the Bank”. You unpack the details about this account, in other words, you tell a story.

You inform me that you own that bank account. It is in your company name. You can show me documented proof that you own it.

Is it the correct amount? You could pull out a bank reconciliation showing me your balance in the bank on that date, less cheques that haven’t cleared the bank yet, and deposits of cheques that haven’t been deposited at that time.

All facts, all clear. We can all agree on those facts.

Next, Accounts Receivable

Now you show me a number on your Balance Sheet that says – “this is how much my customers owe my business”.

Again, is this a true story? I don’t know yet. So, to back it up, you show me your accounts receivable list and that includes all the details of each customer and how much they owe you.

You also tell me that you have reviewed each item carefully and determined that they are good payers, and they all will actually pay you.

I may ask some questions – especially about the ones over 90 days.

Why?

Because it is well known that the older the account the less likely it will be of being collected.

Yet all of these are verifiable facts. I could see over the next few weeks how these accounts receivable are converted into cash.

Inventory

What is inventory?

Inventory is stuff on hand that you either bought from a supplier or built yourself that you will re-sell.

You show me how much your inventory is valued at.

Is it a true number or a phony number?

I don’t know. You need to show me your inventory. Show me the details – how many of this item and how many of that item? What did you either pay for it or what did it cost you to manufacture?

Can you sell it for that much I ask?

You tell me that yes, plus a profit, and that you even reduced the cost on some items to the actual sales value you believe you will get.

Do you start to see how this story is a story you can check up on by asking for more documents or even looking on shelves of widgets and count them?

Can you also see, that by writing things down, this becomes a conservative story?

When I say conservative, I mean you have taken the trouble (this is an accounting principle, by the way) to reduce the cost of certain items of inventory that you feel are worth less than what their cost is.

It is kind of like “under-promising” and “over-delivering”.

Fixed or Capital Assets

Next, I look on your Balance Sheet and see you have bought some capital items – things that do have a future value.

Why do they have a future value? Because they are things that will last longer than 1 year.

We can all agree that usually computers, cars, buildings and furniture do last more than 1 year.

You can show me these physical assets. You can pull out legal purchase agreements for what you bought. You can show me invoices.

You will also be depreciating those assets over the next few years based on your estimate of how many years they will last.

Although, the number of years they will last is unverifiable in reality, you, again, have taken a conservative approach. You have reduced their value by your estimate of the wear-and-tear, and reduction in value that occurs over time.

Goodwill and Other Intangibles

The next items in the asset section of your Balance Sheet are intangible items, like goodwill.

Goodwill – what’s that?

Great question! If you made it up, as in, this is the extra value my business has over and above it’s net assets that I can sell it for, then it is a real fairy story you are telling me.

If, on the other hand, you bought that goodwill, you actually paid for it to a third party, that is another matter altogether.

Now, you are able to show me purchase agreements and dollar figures.

Does it mean that it is worth what you paid for it? Sorry to say so, but likely not.

However, it is verifiable in that I can see an actual invoice.

To determine its actual real-life value, I would hire a business valuator to come in and assess the entire business and let him or her place a value on the goodwill.

Deferred Charges

Ok, dear reader, you have been very patient, and now for my rant…

Deferred charges are what exactly? Again, they are things that you would normally expense, however you have decided to defer them to some point in time in the future when you will write them off.

How did you determine this?

By assumptions. Now, the story takes a left turn.

For all the other items above you can show me verifiable documents for what you purchased. You can show me physical stuff even. You can show me bank statements, customer lists, and so on.

Now, you are telling me that these items – these deferred charges, or expenses, have some future value.

How did you determine that value? You tell me that you invested extra labour that will result in higher customer retention and that that cost can be matched to future revenue.

You have no agreements, no proof, no ability to validate the actual time frame involved.

Will it benefit business for 5 years? 10 Years? 1 year? You get to say because it is not based on anything real.

This is the opposite of the conservatism principle.

This is inflation. Inflating your assets to show a value that you cannot prove.

Increasing your income by reducing your expenses.

This is why a non-conservative approach to accounting creates monkey business. And it can defraud lenders and investors.

By the way, there are times you would defer expenses by following the conservatism principle. An example would be start-up development costs when a building is under construction. These would be capital costs in nature, and rightly placed on the Balance Sheet.

So, the moral of the story in this: whichever political party you support, in accounting always be conservative, and know that every number tells a story!

Thanks for reading…